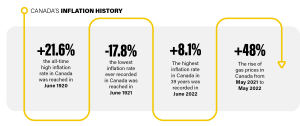

The Canadian Consumer Price Index — a commonly used measure of Canadian inflation — continues to climb, reaching 8.1 per cent in June. This was the largest yearly increase since January 1983 and up from a 7.7 per cent gain in May. Statistics Canada reported that the price of gasoline was a major factor. Gas prices rose by 12 per cent in the month of May alone, and are up by 48 per cent compared to where they were a year ago.

Inflation has surged, thanks to disruptions to supply chains and pent-up consumer demand for goods that emerged when local economies reopened in 2021. Plus, the unprecedented government cash handouts probably added fuel to the inflation fire.

Much of that extra cash injected into the financial system had to go someplace, and in our corner of the world, it moved into real estate and the stock market. Naturally, both assets skyrocketed, but as prices rose, that extra cash produced a domino effect in the housing markets, creating blind bidding wars and possibly squeezing out local buyers.

The Bank of Canada Raising Interest Rates

The Bank of Canada (BOC) has started to raise short-term interest rates, after holding them at record low rate levels during the pandemic. The question that has everyone on pins and needles is: How much will rates end up being raised? Prices and inflation are driven by three factors: producer prices, employment and disposable income.

Producer prices are related to the costs of construction, manufacturing and agricultural inputs; think copper, iron ore and fertilizer. Unfortunately, with supply disruptions affecting primary industries, many producers have been forced to raise prices. Given the horrific war in Ukraine and changing climate conditions affecting farmers globally, expect higher food prices.

On the employment front, Canada is facing a labour shortage and it’s a Catch-22 situation. Boomers are retiring in record numbers, and millennials and Gen Zs seem to prefer a better work/life balance. To compound matters, governments are already running record negative budgets and are reluctant to add to future deficits. Two solutions are possible to solve the labour shortage. The first is higher wages; the second is increasing skilled immigration, both of which will exacerbate the housing crisis and, by extension, inflation.

Disposable income is tied to employment and retirement assets; you just have to subtract ever- higher taxes on income. Nominally, the number is on the upswing, but with inflation running hot, Canadians are losing ground. The question is: Where will it go from here? History may provide some clues.

Hold on: Could be a Bumpy Ride

The inflation rate in Canada averaged 3.11 per cent from 1915 until 2022 but reached an all- time high of 21.60 per cent in June of 1920 and then a record low of -17.80 per cent in June of 1921. That was a century ago, but these figures clearly indicate rapid and potentially violent swings.

Today’s inflation rate stands at a 39-year high of 8.1 per cent. Not quite as bad as some historical periods, but these are rates many Canadians have not experienced in their lifetime. Furthermore, the BOC has a mandate to keep medium-term inflation within a range of 1 per cent to 3 per cent with a midpoint of 2 per cent averaged over six to eight quarters. We are not even close.

For business owners, with rates of inflation growing faster than personal income increases, customers are worse off. This usually leads to lower levels of consumer spending and a fall in sales for businesses. But it takes time, and when input costs like oil, gas, lumber or steel rise, it becomes entrenched into the products we buy.

For business owners, with rates of inflation growing faster than personal income increases, customers are worse off. This usually leads to lower levels of consumer spending and a fall in sales for businesses. But it takes time, and when input costs like oil, gas, lumber or steel rise, it becomes entrenched into the products we buy.

It’s very difficult to bring them back down without causing the economy to crash. Or worse yet, prices remain stubbornly high and economic growth falters, a.k.a. “stagflation.” But with current inflation above 6 per cent, the BOC has started to drain liquidity from the financial system by raising short-term rates to help cool demand and steady the economy.

Unfortunately, we are in the early innings of the inflation game. But, as rates rise, the cost of capital will erode profit margins. And, as we all know, banks tend to reduce credit lines and/or increase their lending rates or demand more collateral to secure their positions. Remember back in 2008 when secured lines of credit went from prime” to prime plus one?

Business owners will likely reduce inventories to lower their finance costs, but if the BOC moves too aggressively, businesses already struggling from COVID shutdowns could go bankrupt. If they don’t, the implied value of their businesses will naturally fall.

One could argue we are in a new paradigm, and supply disruptions will be short-lived as countries including Canada abandon global trade in favor of domestically produced goods. Both businesses and consumers would also adjust to higher–but not rising–interest rates leading to stable prices and a safe investment environment. In this case, the decline in value of small businesses would likely not be as severe.

The big question that remains centres around how long the inflation period will persist and whether it becomes a precursor to a recession. Central banks will have to thread the needle very carefully if they intend to keep the economy recovering but not allowing inflation to erode that growth and set us back into an economic slowdown … in other words “stagflation.”

Historically, central banks have not fared well during inflationary cycles, especially when hit with exogenous factors beyond their control. In this case, the combined effects of COVID are hamstringing supply chains coupled with Russia’s invasion of Ukraine.

Both could last much longer than current estimates, which will only serve to increase inflationary pressures. Business owners tend to reduce and protect. Or, we could adopt a Serengeti-like philosophy, especially if local businesses are to survive. Automate as much as you can and train and retain what you cannot. ′

Steve Bokor is a Chartered Financial Analyst® and licensed Portfolio Manager at Ocean Wealth. He has over 30 years in the industry and hosts the Bokor in the Morning podcast and Your Money on Chek News.