Phil Nicholls has operated his 2:18 Run store in Victoria for over 30 years. Two decades ago, crime was more of the “old-school break and enters,” he says. But in two separate 2024 incidents, savvy crooks made off with thousands of dollars of merchandise. After a 2021 crash where a woman drove her vehicle into his store window, his insurer pulled its coverage. Add the smash-and-grabs, and it became difficult for him to secure insurance at all — or exceptionally expensive to do so.

“One [insurer] fired me, essentially,” he says. “When you get these constant hits, insurers won’t insure you.”

Following his second 2024 B&E, Nicholls started to look for solutions beyond insurance. He found it in Riot Glass, a manufacturer of bullet- and smash-proof glass. In September, an Ontario-based Riot Glass crew installed two new storefront window panels, about 50 square feet total, at a cost of about $125 per square foot. “This will stop a 9-mm bullet,” Nicholls says of the clear glass. “If you throw something at it, it bounces back at you.”

Nicholls also managed to get a new insurer and the company, unsurprisingly, thinks the Riot Glass is a great idea. He says other businesses are considering the product. “I didn’t want bars on windows. I’m not ready for that look.”

Nicholls isn’t alone in his bar fight.

Even though the commercial insurance industry offers a wide variety of products, business owners are increasingly finding themselves either under-covered or even not covered, due to cost. As crime, weather events and rising costs further affect the bottom line, local businesses like Nicholls’s are finding workarounds. And insurance businesses themselves are having to adjust to a changing business climate.

Premium Hikes a Worry

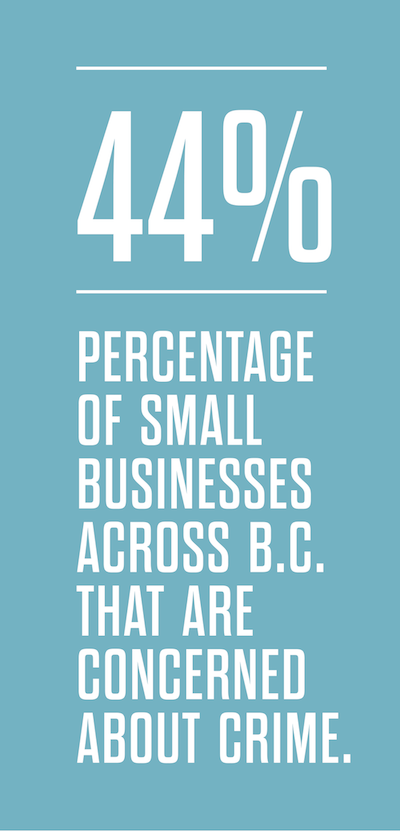

Across B.C., 44 percent of small businesses are concerned about crime, says Michelle Auger, a senior policy analyst with the Canadian Federation of Independent Business (CFIB). Yet, only 15 per cent of businesses always make insurance claims following a crime incident, with those in professional services (six per cent) and hospitality (11 per cent) being the least likely to do so. The main reasons for not reporting include worry over potential increases in insurance premiums (82 per cent), how much time the process takes (40 per cent) and the complexity of claim requirements (29 per cent).

Insurance costs have become the top concern for 68 per cent of those business respondents, up from a historical 49-per-cent average. Tax and regulatory regimes and wages are No. 2 and No. 3, respectively. “Insurance has always been a cost pressure, in the top three, but to be number one is new,” Auger says.

A significant drawback is that when businesses pay heavy insurance costs, it limits reinvestment in the company. The lack of available funds means that spending is restricted on items such as staff, training or equipment and technology upgrades.

A significant drawback is that when businesses pay heavy insurance costs, it limits reinvestment in the company. The lack of available funds means that spending is restricted on items such as staff, training or equipment and technology upgrades.

While a CFIB survey found that 84 per cent of businesses had not filed an insurance claim in the last 12 months, half of Canadian business owners experienced an increase of 10 per cent or more in at least one of their insurance premiums over the same period.

Ken Featherby is well aware of crime’s effects on business. Featherby is a commercial property manager and owner of NAI Commercial in Victoria, which includes the Douglas Shopping Centre among its properties. With over 25 years of Victoria experience, he’s witnessed the steep rise of insurance rates, based not only on risks but on the continued acceleration of property values. The structure of commercial leases plays a role in tenant insurance. Two rents are built into tenant leases. There’s the base rent, which is the landlord’s income and then the triple net costs, which cover items such as the mortgage, property tax, management fee and insurance.

Ongoing incidents at the Douglas Shopping Centre illustrate how crime and vandalism are being embedded into commercial leases. At least five or six times per year, windows are smashed at the mall, Featherby says. The damage isn’t for theft, but for kicks. “They’ll throw a skateboard through the window,” he says. The management company pays the cost of repairs and those costs are passed, via triple net, to the tenant.

In the seven years since the nearby former Tally Ho Motel was converted to supportive housing, insurance costs have jumped by about $150,000. Because the deductible cost is so high, claims are often not made, Featherby says. Instead, tenants are having to pay an additional $2 or $3 per square foot just for security. One of the Douglas Shopping Centre businesses paid an extra $25,000 for security in one year.

Insurance has not been the magic bullet.

But there are ways, such as Nicholls’s Riot Glass installation, to address insurance costs. Auger’s advice is to seek expert advice. The CFIB reports that 80 per cent of businesses rely on a broker for assistance. “It’s a complicated industry,” she says.

Varied Insurance Needs

While there are roughly 200 companies providing insurance in Canada, with each one offering hundreds of options, Auger says that 71 per cent of Canadian small businesses are covered by three companies. Yet, small businesses cannot be treated as a whole, Auger says. A restaurant, small office or transport company all have much-varied needs. Despite the variety of enterprises, three types of insurance are most often purchased by businesses: general liability; property and auto; or crime.

The national director of consumer and industry relations for the Insurance Bureau of Canada (IBC) understands the many demands placed on a business owner, who may be acting as company janitor, driver and boss. But given the risks to businesses, from employee theft to fire, they should not forgo coverage. “If a business doesn’t have coverage, what are the financial implications?” Rob de Pruis asks. A flooded store could end the business. A malicious lawsuit could ruin a reputation.

A 2024 TD Insurance survey of Canadian businesses found that almost one in five small business owners believe their biggest challenge is an interruption in their business, yet almost 40 per cent of them don’t have business insurance. Of those, nearly 40 per cent said they didn’t think they needed it and 30 per cent believed it’s not worth buying because they have zero employees. Some wanted business interruption coverage, but the cost, at around $2,000 per year for a one-person business, was too much for solo owners.

De Pruis recommends that owners work with one of the hundreds of insurance representatives in B.C.

Brokers represent many insurance companies while agents usually work for a specific company. Products can be tailor-made, but wading into the insurance pool can get very confusing very quickly, de Pruis adds. Costs vary according to the plans, and can range from a lowly $50 per month for a single owner/operator enterprise up to thousands per month for a tech-reliant law firm. Business owners should make time to do market research and really understand what’s in their policy.

De Pruis recommends that, when buying insurance, a business should insure for risks specific to their business. For instance:

- A storefront enterprise has public liability risk and needs protection from third-party liability claims, such as a customer falling or even the threat of sexual harassment charges.

- Commercial property insurance pays for damage or loss at a business premises, as well as loss of inventory or property.

- Errors and omissions insurance protects against claims due to a mistake or negligence made by a business or its employees.

- If there’s a mortgage on the business premises, insurance is mandatory.

- Commercial auto insurance covers mishaps in business vehicles.

Home-based businesses present different needs, de Pruis says. In some cases, home insurance can have added coverage for the business. And there are commercial policies for homes, such as a landlord who rents space in their premises, i.e. holiday rental or time share.

Then there are specialty areas. Cyber insurance, which has proliferated in the last decade, addresses the increasing risk of cyber attacks and hacked accounts. Smaller companies can be targeted due to the perception they have less robust systems and vulnerable employees.

And like many areas of our lives, artificial intelligence’s tentacles may entwine a business. The IBC’s 2024 Cyber Security Survey reports that 65 per cent of business owners are concerned that AI will make it more difficult to defend against cyber risks, yet only 18 per cent have insurance against an attack.

Another specialty product is business interruption insurance, which covers revenue loss due to causes such as fire, flood or cyber attacks. There’s even pandemic coverage, which also addresses loss of revenue. Throw in coverage for key persons, importers, terrorism, pollution, intellectual property and crime, and the range of policies — and costs — can be vast.

Catastrophic Weather Issues

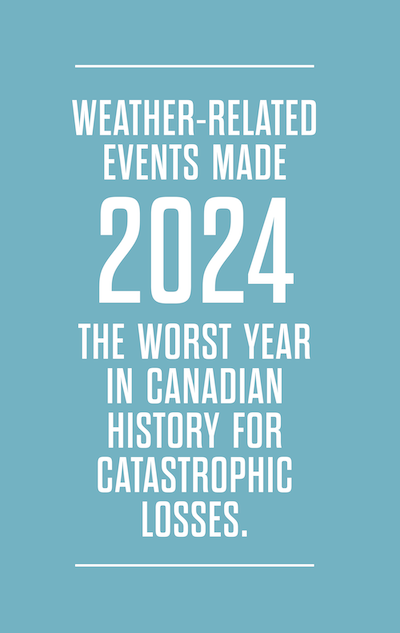

It’s not only crime that’s affecting insurance rates. Weather-related events made 2024 the worst year in Canadian history for catastrophic losses, says Luke Mills, a commercial insurance broker with Acera Insurance (formerly Megson FitzPatrick).

It’s not only crime that’s affecting insurance rates. Weather-related events made 2024 the worst year in Canadian history for catastrophic losses, says Luke Mills, a commercial insurance broker with Acera Insurance (formerly Megson FitzPatrick).

The Calgary hailstorm, Jasper wildfire and flooding in Quebec and Ontario combined to total over $8 billion in losses. “There are no climate-change skeptics in the insurance industry,” says Mills.

In B.C., businesses operate under the ominous trifecta of fire, earthquake and flood risk. For earthquake coverage, the deductible amount has risen substantially in B.C. Unfortunately, the province doesn’t provide government support for coverage, unlike other earthquake-prone jurisdictions, such as Japan, Chile and New Zealand, Mills says. He also notes that substandard government flood mapping is leading to insurance companies creating their own flood maps to set rates.

It’s not just climate change heating up losses. Where buildings are situated and how they are built become significant factors. “And construction inflation is really driving insurance costs,” Mills says. The cost to replace damaged premises rose about 15 per cent throughout 2024, meaning that insurers have to put aside more money to cover ongoing increases. “But insurance companies are innovating and getting better data to insure property against risk, making properties more resilient.” One example is upgraded bylaws around seismic construction.

Amid the bleak landscape, one way a business could reduce its high insurance cost is to ask if its insurance company offers free advice on how to mitigate risks. “It’s not an expense to clients, it’s an expense to insurance companies,” Mills says. A “loss-control assessment” could recommend actions such as keeping cooking equipment clean, ensuring fire extinguishers are not past their due dates, eliminating tripping hazards or removing graffiti. Businesses should also request discounts if improvements have been made, such as adding security cameras or cybersecurity training.

“But crime prevention is a tough one,” he adds.

Natural Disasters Hit Home

Terry Dodsworth has 30 years of experience, advising businesses about their insurance. The last 22 have been with AON Canada, where he is managing director of commercial broking. As a national insurance broker, AON staff get down to fundamentals with clients, addressing assets and coverage for various risks.

Last year’s numerous natural disasters hit home for many clients. “Smaller Victoria businesses would see it [premium jumps]. It was a double hit — reinsurers’ exposure and geographic exposure,” Dodsworth says.

It would be normal to assume that insurers are under heavy financial pressure during a costly cycle, which occurred from about 2020 to early 2024, but Mills says that insurance companies themselves buy insurance — the reinsurance. Invested monies yield profit for the reinsurers, who operate in a globally integrated market. The money cushion prevents insurers from levying very high premiums on clients, yet doesn’t completely soften the blow.

About five years ago, the landscape was more challenging, Dodsworth says.

Rates and deductibles had substantially jumped. “Insurers were very picky about the risks they were taking. Businesses couldn’t get insurance for what they wanted,” he says. Since late 2022, with more available capital in the market, the situation has improved, albeit for clients who aren’t seeing a lot of activity.

Dodsworth has three tips for businesses about to buy or renew their policies.

- Begin researching options at least one month before your policy is about to expire.

- Have at hand very solid information about your business, such as a statement of assets, what the business does, production rates and revenue.

- If your business has had prior claims, what was learned? What has been done to address the cause of the claim?

As Mills says, “Insurance is reactive. It comes into play when something bad happens. People buy it, hoping they never have to use it. Some business owners have a high risk tolerance. Some are OK with high deductibles.”

When facing so many undermined and uncontrollable events, insurance is one item where determined control, at a cost, can be ensured.