Are you eagerly awaiting retirement — or dreading it because of financial worries? Our Money columnist explores strategies to help you plan a more secure future.

Whether you’re a business owner, an executive or an employee, the topic of retirement doesn’t always bring a sense of well-earned relief and happiness. Instead, worries creep in as we transition from a life of known routines, steady paychecks and paid vacations to a life full of uncertainties. Even those individuals with gold-plated, indexed government pensions have been known to express doubts about retirement. “What happens if I get a debilitating illness? Who will take care of me? Will I outlive my retirement capital?”

If you’re a baby boomer, you may be nervously focusing on an imminent retirement or have recently made the transition. Indeed, boomers have been the focus of much of the investment world — and its cheesy financial-planning commercials — for years. As they begin to hit 65, unexpected changes and market volatility can cause many boomers to reassess their retirement dates. Many retirees simply cannot be exposed to severe — or even modest — market losses. They need to protect their savings in a cost-effective manner.

Fortunately, there are investment strategies that can minimize or eliminate most prospective retirees’ financial fears. But you need to know the magic number, which is different for everyone. First, contact Services Canada to determine your CPP and OAS future benefits. The current maximum benefit starting at age 65 is $13,300, or $26,600 for dual income earners. If you add in another $6,800 each from OAS, a working couple will have a combined income of $40,000 in retirement.

CPP can start as early as age 60 or be deferred until 70 with benefits reduced for each year starting before age 65 and increased for each year after 65. The decision of when to take CPP depends on your other sources of retirement income (government or corporate pensions,) health and employment satisfaction. I have clients who work into their late 70s and a few who still enjoy working in their 80s. In general, individuals will be further ahead after age 82 if they defer the start of CPP until age 70.

Get the Most Out of Your Savings

The goal is to maximize your after-tax income. If your retirement income from investments and pensions exceeds your current spending requirements, delay converting your RRSP into a RRIF until age 71 to defer the tax bite.

Fully fund your TFSA from non-registered assets (you don’t have to fund it with cash), but take care on the attribution rules for gains and losses. The cumulative limit is now $52,000, and at 5 per cent that could generate another $2,600 per year tax free.

Some retirees will want to convert as many financial uncertainties into certainties as they can. Perhaps take advantage of tax-efficient investment vehicles that give you peace of mind. Two strategies are to purchase life annuities or T-series mutual funds. Both are designed to provide a steady tax-advantaged income for life, or 20 years or more.

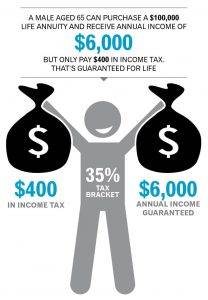

For example, a male aged 65 can purchase a $100,000 life annuity with a 10-year guarantee that will generate monthly income of about $500. More important, the taxable portion is only about $95. Put another way, an investor in a 35 per cent tax bracket will receive annual income of $6,000 but only pay $400 in income tax. That’s guaranteed for life.

For example, a male aged 65 can purchase a $100,000 life annuity with a 10-year guarantee that will generate monthly income of about $500. More important, the taxable portion is only about $95. Put another way, an investor in a 35 per cent tax bracket will receive annual income of $6,000 but only pay $400 in income tax. That’s guaranteed for life.

Many mutual funds offer a T-series distribution. A $100,000 investment will generate $6,000 annually and the taxes will be deferred for about 17 years, with future income considered capital gains. However, in the case of the mutual fund, adverse financial conditions could affect the monthly income in later years so a degree of caution is warranted. Consult with a professional advisor.

Protecting Investment Portfolios

Even financially secure retirees should not be exposed to severe — or even modest — market losses. If you currently have a large investment portfolio, in stocks, mutual funds or Exchange Traded Funds (ETFs), there may be a need to protect your savings in a cost-effective manner. There are a number of alternatives that can provide downside protection. One of them is “protective put options,” which I don’t have enough room to adequately explain here, but you may want to ask your financial advisor about them.

When it comes to your investments, do not try to make up for below-average returns by investing more aggressively. Juicing your retirement portfolio dramatically toward more volatile-growth stocks does have the potential to generate bigger gains — but also more risk, and this is where those protective put options may be of use. Similar caution applies to bonds. Moving high-rated, short- and intermediate-term bonds to high-yielding junk bonds or long-term issues may seem like a sure-fire way to boost returns in a low-interest-rate environment.

Until interest rates tick up, which seems likely given that the Federal Reserve has signaled continued “gradual increases in the federal funds rate,” bond prices will fall — and bonds with the longest maturities will generally get hit hardest.

You know your number … now you know one way to protect it.