A friend of mine had a successful retail surfwear company in Vancouver quite a few years ago. He was scaling by increasing sales. His product was sourced from Australia, which meant prepaying for inventory. That inventory would be put on a ship and take about four weeks to get to the Port of Vancouver. He had a brick-and-mortar store in a desirable, but expensive, location. The company was thriving. Revenues were growing at a fast pace. The income statement was healthy. Margins were solid. Despite all this, cash flow was tight, and getting tighter. Why was the growth model not working?

Like my friend, maybe you’ve reached a plateau and decided to scale your venture. You have considered the alternatives for growth, including:

• Increasing sales: by expanding the customer base, increasing the frequency of purchases, upselling and cross-selling to existing customers.

• Raising prices: by increasing the value proposition of your product or service and/or improving its appeal through marketing and advertising.

• Expanding into new markets: by entering new geographic markets, launching new products or services or targeting new customers.

• Mergers and acquisitions: by acquiring other companies or merging with them to expand the company’s reach, customer base and product offerings.

• Improving operational efficiency: by streamlining processes, automating tasks and reducing costs, which can increase profitability and allow for reinvestment in growth.

It’s important to note that each company’s situation is unique, and the best approach will depend on the specific strategy, economic and competitive context, and goals.

The Cash Conversion Cycle: What Is It and Why Does It Matter?

The cash conversion cycle (CCC) is a measure of how quickly a company can convert its investments in inventory and other resources into cash. The CCC helps to determine how efficiently a company is using its resources, and it can be an important indicator of a company’s financial health.

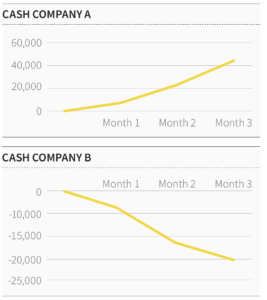

Let’s take an example, where Company A collects prepayments from customers for its product, and uses its 30-day credit terms with suppliers. At Company B, inventory is paid for a month in advance, and customers have 30 days to pay (see chart on page 70). Assuming a 50 per cent margin and starting cash of zero dollars: In Company A, cash keeps growing and growing. Company B has a hole that keeps growing. You need proper financing to cover rapid growth with a longer cash conversion cycle. You also need financing, or savings, in a company with large, stepped fixed costs, such as a lease for additional space or adding more employees before they can generate revenue.

Danger Ahead!

Back to my friend’s surfwear company. Remember that revenues were growing; the income statement was healthy. Suddenly, he reached the limit of his credit, the bank called his debt, and his company went bankrupt. I met him when he was taking courses to make sure that it never happened to him again. His company looked great on paper. What went wrong?

Cash flow! He was Company B. He was getting mixed signals. On one hand, revenue was growing and this felt like success. He didn’t understand what was happening to cash, and felt sure that as he continued to grow, that the cash situation would right itself. It likely would have, given adequate financing and more time. If he had forecasted his cash flow needs, obtained additional financing and kept his bankers in the loop, he might have survived this period of intense growth and still be running that surfwear company to this day.

What can we learn from his experience?

How to Scale Effectively

Cash flow tracking, forecasting, and cash management are critical when scaling your company. Cash management includes tracking and forecasting, plus deciding how much cash to hold, investing excess cash, and managing the company’s short-term debt, such as lines of credit and commercial paper, to ensure that the company has access to cash when it is needed.

Expert tip: Treat cash flow tracking and forecasting as a hand-in-hand learning experience.

Forecasting cash flows and then tracking actual cash, to check your precision, helps you become skilled at determining future financing needs. Cash flow tracking and forecasting together are a learning exercise. If you start forecasting before you scale, you develop the skill to predict cash needs with some accuracy.

This doesn’t have to be a technical or complex activity. A simple Excel spreadsheet, with cash inflows (revenue, financing) and cash outflows (expenses, capital purchases, financing such as loan principal repayments) and determining the ending balance, will do the trick. As you track the actual cash inflows and outflows against your initial forecasts, you will get better at forecasting.

Determine the time range that each Excel column should cover: you can break down your cash flow forecast by month, bi-weekly, weekly or daily. If your payroll is a significant expense, forecast biweekly. If the lease cost for your space is your most significant expense, then monthly tracking might suffice.

Expert tip: Maintain cost discipline during growth.

In this context, cost discipline means making conscious decisions about spending. There’s lean, and there’s mean — be lean, not mean. Scaling is an important time to keep an eye on costs, as it’s easy to take on high, recurring costs and weakening margins, when the focus is growing revenues. Maintaining cost discipline through a time of growth sets up your company for the next phase, once the revenue growth is achieved. It is harder to change gears and reduce costs; it is easier to maintain cost discipline and not have to make significant cuts at the end of the transition.

That said, balance cost discipline with culture and employee retention. Ensure that everybody on your team is supported during a very intense period.

Expert tip: Set up financing well before you need it.

Get some financing in place. Scaling is often more difficult than anticipated, and there can be bumps on the road. Having your financing set up in advance allows you to focus on solving problems rather than the distraction of setting up financing. Do that work before entering the growth phase. Remember: Bankers do not like surprises and the best time to negotiate is before you need the funds.

If we go back to my friend’s surfwear company, had he forecasted and recognized the oncoming cash crisis before it occurred, he might have had alternatives to avoid bankruptcy, including:

Slowing growth, and managing it within existing financing;

Arranging additional financing to bridge the growth phase.

Mia Maki is an associate dean, faculty outreach, at the Gustavson School of Business at UVic; a professor of finance, accounting and entrepreneurship; and a principal at Quimper Consulting. Maki has helped raise over $50 million for international initiatives, including acquisitions, strategic partnerships and joint subsidiary creation projects.