Student loans, credit cards, bills, budgets, housing, investments, retirement — as a young professional, you have a lot to think about. Throw inflation, a high cost of living and exorbitant rental costs into the mix, and money management can seem overwhelming.

Despite these challenges, there’s a lot you can do to set yourself up for the future. We turned to two financial planners — both of whom are young professionals — for their advice for managing your loans and credit cards, figuring out if your rent’s too high, saving for retirement, budgeting, thinking about your finances holistically and long-term life planning.

Student Loans

According to data from Employment and Social Development Canada, post-secondary students graduated in 2019 with an average federal student loan balance of $13,367, and that’s not including the amount they owed to provincial and/or private sources. Paying off that much can be a daunting task.

As of February 19, 2019, B.C. eliminated interest charges on government-issued student loans. And as of April 1, 2023, the federal government permanently removed the accumulation of interest on Canada Student Loans. Interest on loans from private institutions varies.

If you have a federal or B.C. student loan, you have to make minimum monthly payments until you’ve paid it off. And that also applies to most private loans. But should you stick to your payment schedule or pay off your loan as quickly as possible? That depends.

If you anticipate needing to apply for a loan for, say, a first home, you may want to prioritize paying back your student debt as quickly as possible. When lending, banks can look at your cash flow as a measure of whether you can pay them back. If your student loan is a significant drain on that, banks may not lend you as much as you would like, says Mark Lotocky, the owner of financial planning company The Dixon Davis Group.

It’s also important to factor your emotions into your decision, says Josue Dubon, a partner and wealth mentor at financial planning company DesignWealth. If your student loan is a source of stress, it may be in your best interest to just pay it all off.

However, if paying off your loan quickly means sacrificing your standard of living, you may want to stick to your payment schedule, says Lotocky. For example, doubling monthly payments may mean you can’t go on vacation or out for an evening with friends.

Also, by sticking to your minimum payment, you can invest any extra money you would have used to pay your loan back quickly, say Lotocky and Dubon. That only applies if your loan is interest-free or if investment interest rates are higher than those attached to your loan. For example, if you have a private loan with an interest rate that exceeds that of possible investments, it doesn’t make sense to invest because you’ll be losing money, says Dubon. Instead, it may be best to pay off your debt quickly to prevent it from ballooning. It’s important to note that your situation may be more complex, so contact your bank or speak to a financial adviser to find out if investing is right for you.

Credit Cards

According to credit reporting agency TransUnion, in the second quarter of 2023 Canadian consumers held on average $4,185 in credit-card debt. “When you’re young and you’re getting used to money,” says Lotocky, “it’s really easy to overspend,” a problem compounded by high interest rates.

For example, if you owe $250, at a 20 per cent interest rate, you’ll owe $275 in six months and $304 in a year. That doesn’t seem like a lot, but think about it on a bigger scale. If you owe $5,000, at a 20 per cent interest rate, you’ll owe $5,518 in six months and $6,089 in a year.

One of the best ways to avoid that is to pick a credit card with a limit that you can afford to pay off every month, says Lotocky. He recommends that after paying your bills, buying groceries, investing and saving some money for the future, whatever’s left that you’re willing to part with, use that as your limit.

Lotocky also advises that if you find you’re always overspending with your credit cards, you may want to get rid of all but one of them. For example, if you can only afford to pay back $500 every month, it doesn’t make sense to have four cards with a $500 limit — if you max them out, the money you’ve put aside to pay off your debt won’t cover the $2,000 you’ve spent.

Rent

Dubon and Lotocky agree that spending approximately 30 per cent of your income on rent is a good rule of thumb. But housing is getting increasingly expensive in Greater Victoria. In 2022, you needed to earn at least $34.85 per hour to afford a two-bedroom apartment in Victoria, without spending more than 30 per cent of your income, according to the Victoria Foundation’s 2023 “Vital Signs” report.

If you spend more than the recommended limit, that doesn’t necessarily mean you have to move cities or apartments — you may just have to cut back in other areas of your life. Buy bulk foods instead of shopping at boutique grocers, go on fewer weekend getaways, take the bus instead of driving — it’s all about balance. “As long as you’re working towards long-term goals and can still manage to put something away towards that … and your day-to-day life is decent,” says Lotocky, “then your rent isn’t too high.” On the other hand, Dubon says that if, after cutting back, you’re losing money or don’t have enough to live on, you may need to find a cheaper apartment.

Retirement

If you’re strapped for cash, it’s hard to think about putting money away for the future. But there are benefits to saving for retirement early in life.

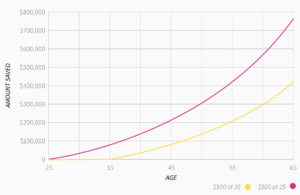

For example, if, at 25 years old, you start investing $100 every month in a Registered Retirement Savings Plan (RRSP) or a Tax-Free Savings Account (TFSA), at a five-per-cent interest rate, you’ll have $15,528 by the time you’re 35. If you continue to save $100 every month until you’re 65, you’ll have $152,602. That’s the power of compound interest. However, if you start saving $100 every month at 35, you’ll have saved $83,225 by the time you reach retirement age.

One hundred dollars might be all you can save right now, and that’s fine. You can always increase your monthly investment later as your income rises. But if you have the means, by investing $1,000 a month at 25, at a five-per-cent interest rate, you’ll have $1,526,020 by the time you’re 65.

But how much do you need to retire? That’s a hard question to answer, says Dubon, because it depends on the lifestyle you want. A modest life will require fewer savings than if you want to spend your winters in Spain and summers on cruise ships. What you want to do in retirement is something only you can answer.

RRSPs and TFSAs are common ways to save for retirement, and every Canadian is guaranteed a pension (amounts vary depending on your contributions) thanks to the Canada Pension Plan.

Active Budgeting and Anti-Budgeting

According to a 2021 Bank of Canada study, on average Canadians have eight bills to pay every month. On top of expenses like groceries, coffee, gas and travel, it’s easy to lose track of your money. Lotocky says active budgeting and anti-budgeting are two ways to avoid that.

Active budgeting involves regularly monitoring how much you spend. You can do this using an Excel spreadsheet, with one column for your income and another for your expenses. Work out a monthly budget (how much you expect to spend on groceries, rent, credit-card payments, student loans, savings, investments, etc.) and regularly compare that number with what you actually spend. This can help you understand your spending habits and where you should pull back.

Anti-budgeting requires that you have three bank accounts. Make sure your paycheques go into an account for static outflows, which you’ll only use to pay for fixed expenses like rent, student loan payments, phone bills and TFSA contributions. With every paycheque, move an allotted amount to a second account for controlled funds, designed to house your long-term savings for everything from travel or emergency funds to money for a new car or house. What’s left, move to the final account, reserved for dynamic spending (day-to-day cash payments that aren’t static). This could include everything from groceries to movies to a night at the pub with friends. Organizing your finances this way can help you keep track of your money, stay on top of your financial obligations and save.

Holistic Thinking

The above advice can help you manage your finances, but equally important is how you think about money. Dubon says that if you look at your finances as silos, you won’t see how the financial decisions you make are connected.

For example, saving lots for retirement now is good in theory, but doing so may mean you won’t have enough money to start your dream business. Or moving to a cheaper apartment may help you save money to pay off your credit bill, but if you have to commute an hour every day to work, you may lose out on gas expenses.

Long-Term Life Planning

More important than any of the insights here are your goals and how you can use your finances to achieve them.

Led by Thomas Gilovich, a professor of psychology at Cornell University, a 2018 survey about peoples’ enduring regrets revealed that 76 per cent of respondents said their biggest regret was not becoming who they wanted to be. Gilovich found much of that had to do with inaction (not pursuing aspirations and goals).

What does that have to do with money? Starting a family, seeing the world, opening a restaurant, pursuing a career you’re passionate about, living free and easy, getting a PhD — whatever it is you want to do, however you picture yourself in the future, a rock-solid financial plan can go a long way in helping you get there, says Dubon.

But first, you need to know what you want. What excites you? What gets you out of bed in the morning? What goals do you have? What do you value? What do you want to contribute to the world? What do you want to leave behind after you’re gone? These are tough questions, but they’re worth giving some serious thought. After all, you have one life — why not spend it doing something you love?

Next Steps

If you’re ready to take control of your finances, a great next step is to check out a few of the many free financial literacy courses available online. For example, the Financial Consumer Agency of Canada offers a 12-part online course called Your Financial Toolkit that covers everything from debt management to fraud protection.

After starting out on your own, if you find you need it, hiring a financial adviser may help you make sense of your finances. Whether or not you seek professional help, this process can cause some stress. Talking to a trusted family member or friend may help you approach your situation with clarity and calm.

Also, know that you don’t need to have it all figured out. But starting to think about ways to manage your finances can help set you up for a happy, prosperous future — one that’s uniquely yours.

The 50/30/20 Rule

Here’s an easy-to-remember rule of thumb for budgeting. Start by taking a look at your paycheque. If taxes are withheld, subtract that amount from your total earnings. Don’t subtract other amounts that may be withheld or automatically deducted, like health insurance or retirement contributions. Those will become part of your budget.

The 50-30-20 rule recommends putting 50 per cent of your money toward needs, 30 per cent toward wants and 20 per cent toward savings. The savings category also includes money you will need to realize your future goals.